Electric car makers including Tesla and BYD have unleashed further discounts and incentives in China in a final push to meet annual sales targets.

Rohm Semiconductor and Valeo have jointly announced a collaboration to design and develop the next generation of power modules for electric motor inverters, combining their expertise in power electronics control. In the initial phase, Rohm will provide Valeo with a 2-in-1 SiC molded module TRCDRIVE pack for future powertrain applications.

Hotai Motor, Taiwan's automotive leader, projected Taiwan's vehicle market will reach 460,000 units in 2024, up from a prior estimate of 450,000 units, citing steady domestic demand and improved production conditions.

Lithium-ion batteries, a cornerstone of modern technology, traditionally rely on cobalt for their stability and energy density. However, cobalt's high cost, environmental concerns, and its concentration in geopolitically unstable regions have raised alarms about supply chain vulnerabilities.

The Chinese electric vehicle (EV) industry is characterized by intense competition as numerous automakers aim to achieve profitability in the face of increasing sales. Xiaomi, with its substantial financial resources, has the potential to disrupt this market.

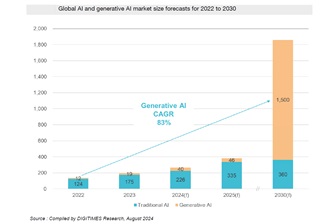

IC distributor Zenitron has broadened its AI product portfolio while deepening its presence in China's automotive industry.

The landscape of the three key new energy vehicle (NEV) markets—China, Europe, and the US—will undergo dramatic changes in 2025. Price competition is expected to continue, driven primarily by government policies across these regions.

Huawei has registered several new trademarks for electric vehicles (EVs) in China, signaling deeper collaboration with Chinese automakers.

The automotive industry is experiencing a significant transformation with the rise of electrification and connectivity. Despite this shift, the ecosystem is still in the process of maturing. The automotive semiconductor industry continues to be largely controlled by well-established suppliers from Europe, the US, Japan, and South Korea, even as companies like Tesla and emerging Chinese players make their mark.

On November 26, BYD announced a directive requiring its suppliers to implement a 10% cost reduction starting January 1, 2025. Following this, SAIC Maxus has reportedly launched a similar initiative, also targeting a 10% cost cut across its upstream supply chain, further intensifying market-wide cost optimization efforts.

Topco Technologies, which distributes silicone and other chemical materials, is optimistic about demand for AI servers, but the outlook for the automotive sector is bleak.

More coverage